March 30, 2026

Partner Content · WithCoverage

Your Bonding Capacity Is Killing Your Construction Pipeline — Here's How to Fix It

You qualified. You bid. You won on merit. Then your surety partner said no. Here's why that keeps happening — and what a better-structured surety program actually looks like.

Every day in construction, contractors lose work they were qualified to win — not because of a failed bid or an uncompetitive price, but because their surety program wasn't built to support growth. Generic brokers set limits conservatively. Carrier relationships stay thin. Nobody positions the financials before they need to be positioned.

The result: GCs, subs, and developers losing millions in work they had the skills and track record to deliver.

Bonding capacity: a growth problem disguised as a finance problem

Most contractors treat bonding reactively — as something to sort out when a project requires it. That's the wrong frame. Bonding capacity determines which projects you can pursue before the first bid goes out. A surety program that isn't built to grow with your business becomes the ceiling on your pipeline.

"Bonding capacity isn't just about the size of the bond — it's about how your financials are presented, which carriers you're positioned with, and whether your broker is fighting for you or just processing paperwork."

WithCoverage was built specifically to solve this. Construction-exclusive, carrier-connected, and proactive — they structure surety programs as growth tools, not compliance checkboxes. The difference between a broker who knows construction and one who doesn't shows up in the bond limits you can access and how quickly you can get them when a project comes in.

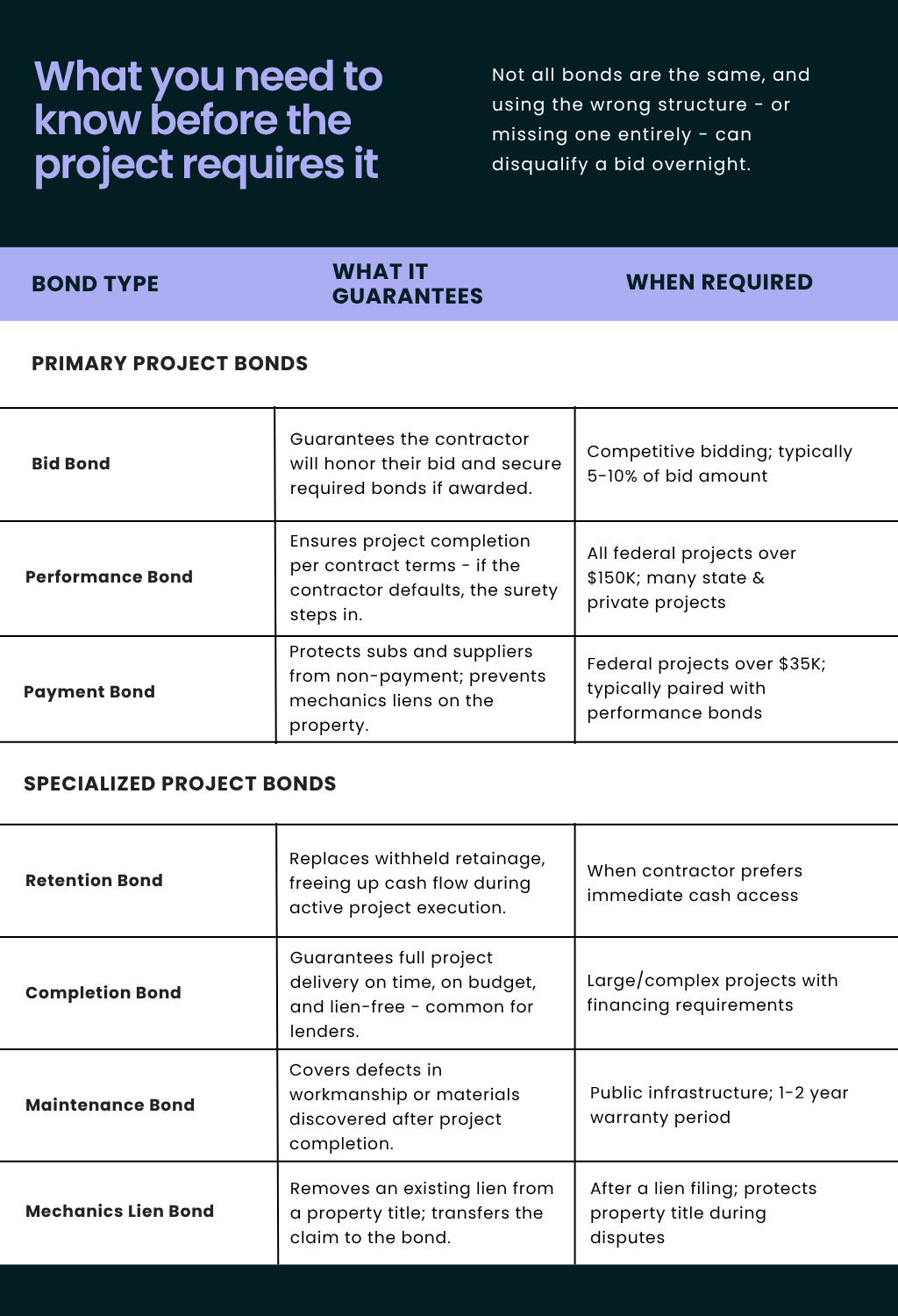

Federal and state bonding requirements

Bonding isn't optional on most public work — it's a legal requirement. The thresholds vary by project type and funding source, and getting them wrong doesn't just cost you a bid. It can expose you to significant liability.

Federal

Projects over $150K

Federal Miller Act

Federal projects over $150K require payment and performance bonds. Projects between $35K–$150K require a payment bond at minimum. Miss this and you're not just disqualified — you may be liable for unpaid subs without lien protection.

State & Private

Varies by state

Little Miller Acts & Private Projects

Every state sets its own thresholds. WithCoverage tracks requirements across all 50 states so you're never guessing. For private projects, bonds aren't legally required but are increasingly demanded by owners and lenders as a condition of financing.

What GCs, subs, and developers should do now

Whether you're a general contractor qualifying your sub roster, a specialty sub chasing larger public contracts, or a developer managing lender requirements — your surety program needs to be proactive, not reactive.

For General Contractors

- Know your sub's bonding capacity before bid day — not after award. Discovering a capacity gap at award creates schedule delays that compound through the project.

- Require bonding commitments upfront to avoid compliance issues mid-project. Lock it in during pre-qualification, not during execution.

For Subcontractors

- Know your single and aggregate limits. If you can't recite them, you're leaving bids on the table.

- Position your financials before bid season. WithCoverage helps you present working capital, net worth, and revenue trends in the strongest possible light — before you need the bond, not while you're trying to get it.

- Don't assume your broker is shopping the market. A non-construction-specific broker likely has limited carrier relationships and can't generate competition on your pricing.

For Developers

- Bonds aren't just a lender checkbox — they pre-qualify your GC and protect your project timeline from the start.

- Pair bonding with insurance strategy so your program is structured without gaps from day one. Siloed decisions on each create exposure in the overlap.

Bonding capacity as a competitive advantage

The contractors who grow aren't necessarily the ones with the best crews or the lowest prices. They're the ones who treat their surety program as a strategic asset — something to be maintained and expanded continuously, not pulled off the shelf when a project demands it.

That means working with a broker who understands construction financing, maintains active carrier relationships, and positions your financials proactively throughout the year. It means knowing your limits before bid season, not during it. And it means having a program that can flex when a large opportunity comes in — rather than one that forces you to walk away from it.

"In today's market, bonding capacity isn't a back-office function — it's a front-line competitive advantage. The contractors who grow are the ones who treat their surety program like a strategic asset."

For certified subcontractors in particular, bonding capacity is often the difference between staying in the $500K project tier and moving into the $2M+ tier. The skill gap usually isn't the issue. The surety gap is.

WithCoverage · Partner Offer

Get Your Complimentary Surety & Bond Analysis

Find out exactly where your bonding capacity stands — and where it could be. WithCoverage's team will review your current surety program, identify capacity gaps, and show you what a competitive bonding strategy actually looks like.

Contact: vin@withcoverage.com · withcoverage.com

Stay Ahead of What’s Happening in Construction

Get monthly insights on sourcing, compliance, participation, and reporting — plus updates on what Tough Leaf is building and learning alongside owners, agencies, and GCs.

Built for Prime Contractors, Government Agencies, and Certified Subcontractors.